39

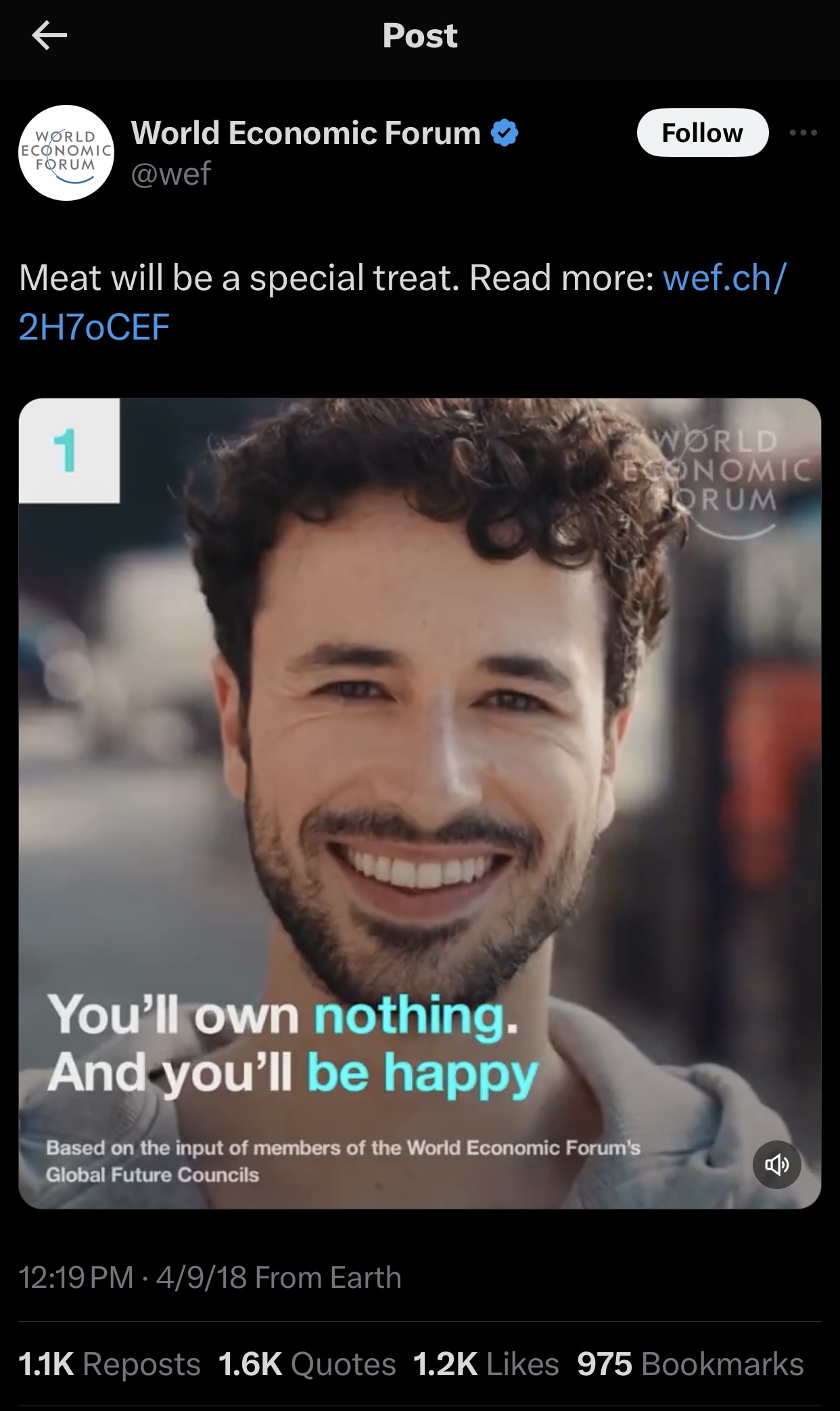

This is from 2018. It is basically the "huffing your own farts" version of bringing back the company town but this time it's neoliberal.

It's still relevant, though, because the economic forces that be were already doing this and have gained ground. For example, the transition from being able to own a home vs. renting your entire life. Included in that is the fact that people who "own" their home are often incorrect about this. In reality, the home was purchased in a loan and you are now paying a bank economic rent (interest) for the privilege. Over time we see the shifts: more people have to rent, they have to rent for longer, and loan terms and worse and worse.