4

16

7

4

14

13

19

14

22

21

23

15

Does the latest Bank of Canada announcement mean it’s go time again for variable-rate mortgages?

(www.theglobeandmail.com)

24

12

The Enshittification of Wealthica

(lemmy.ca)

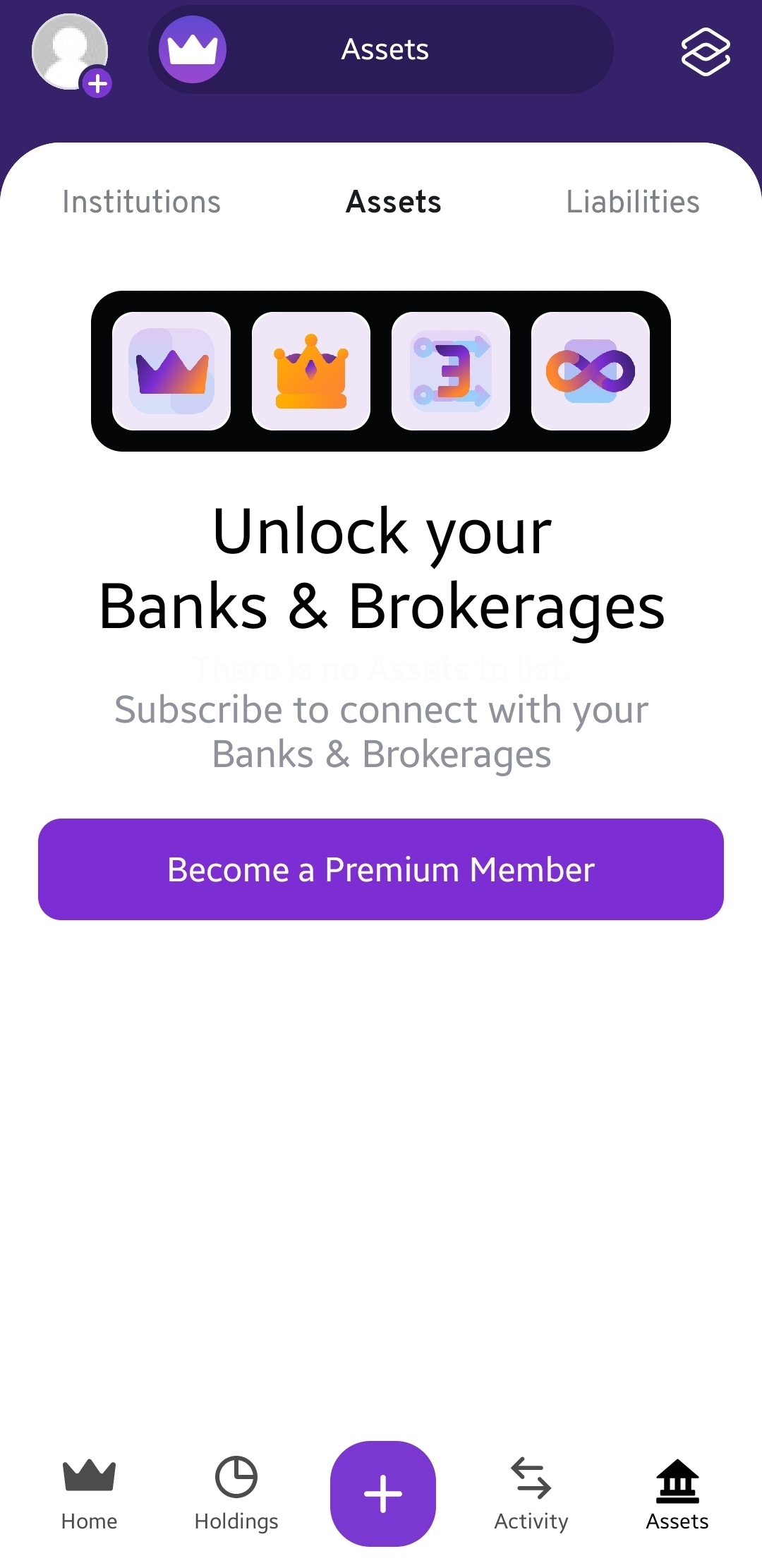

Welp, Wealthica has just been enshittified. Whereas up until recently you could view all your banks/brokerages/assets with updated values, you now have to have a paid subscription.

Anyone know any alternatives? Or do we go crawling back to manual spreadsheets?

view more: next ›

Personal Finance Canada

1167 readers

1 users here now

Come and discuss anything related to personal finance, directly or indirectly, with other Canadians!

founded 1 year ago

MODERATORS