240

How much do Americans actually pay for healthcare?

(pawb.social)

A lot of people simply don't because they can't. It's absurdly expensive because the system isn't designed for people to pay for it out of pocket. If someone doesn't have insurance, they'll either beg the hospital for mercy or ignore the medical debt because it doesn't count against your credit score. Even if they do have insurance, it often doesn't cover a portion of the cost, the insurance is extremely expensive, or both. The people with quality insurance through their employer have it good, but the system expects everyone to have that privilege.

My father has had two heart attacks. The first was a pretty standard one by heart attack standards, required a stint to be put in and two days at the hospital. The cost was ~$40k and after insurance we were left with I think a $4-5k deductible (pretty good county employee insurance). His second one luckily (ha) happened while on the job and required another stint to be put in (he got amazingly lucky, as it was a widow maker of a heart attack) and was covered under his works insurance.

For reference, I'm healthy and in my late 20s, I pay ~$250 a month through my employer's health plan, $25 for an office visit, $500 to walk through the doors of the ER, with a $3k in network deductible ($6k out of network). Believe me when I say you are amazingly lucky to have the NHS.

I had a surgery that ended up costing a few thousand dollars after insurance and we have ok insurance at work.

You're fucked if you don't have insurance, which is common for a lot of the working class.

Depends.

I pay $600/mo for insurance, mid-grade, without using it. Co-pays, medication, or any other medical procedures are all varying costs and extra out of our pockets. Some things are “free”, like vaccinations, and maybe some basic meds might be zero copay at the pharmacy, but it all comes out of the paycheck. Out of network doctor or specialist? Way more.

Things that are not covered are any extra insurance like long or short term disability. Long term care. Psych care. There are some things that cost extra, like ED visits, specialty treatments maybe like dental implants or hearing aids. We pay extra for some of these.

I have a good job, so does my spouse. The monthly costs are in the vicinity of $800 for a family of four, so $9,600 a year. They aren’t big costs, but nonetheless it’s money spent making some insurance company profitable gambling on my continued health. We also take money out of pay for what amounts to a pre-tax bank account that can be used for medical expenses only. You can pay for meds, dental visits, etc. with it. It’s pre-tax, so that’s great, but you don’t get to spend the money if you need it elsewhere.

It’s also all gone if I lose my job - the insurance is through my employer. Too sick to work? Gone. Injury and disabled? Gone. There’s no safety net except Medicare or -aid, and that’s a shitty plan that has all kinds of caveats like Medicaid can essentially take your home as “payment” in certain situations. Completely fucked up.

My insurance constantly gets more expensive and my services become more restricted every time my employer sees fit to reassess their insurance costs.

I would gladly pay a tax (or whatever they call it in countries that don’t call it a tax) in a more level paying field that isn’t tied to my job, that I have to choose what care or physicians I go to because of how much more it costs, or whether I should see a doctor, that doesn’t go to making some assholes rich based on whether or not I get a more costly or denied treatment.

TL;DR: mine is $660/month for health, $42/month for dental

Most folks in the US aren’t aware of how much they pay for health insurance. I live in California, where law requires full time employees (>30 hrs a week, >130 hrs month) be provided some amount of health insurance. The type of coverage varies not just from job to job, but also within the same job the employee must often choose their own plan from several company selected options at varying price tiers and types/amount of coverage. Usually the employee only sees the amount of the monthly cost that THEY are responsible for, which is then automatically removed from their paycheck. What most folks are unaware of is that the employer is also paying some of the cost (which is the part that the law makes them do). The part that makes it extra frustrating to deal with an already broken and overly expensive system, is that the rate paid by employers is negotiated in bulk with the insurance providers. Larger employers (national corporations with hundreds of thousands of employees) are paying much less than an individual or small employer would. This is the one of the largest reasons becoming unemployed is so dangerous in the US. In addition to not having income for food or housing, people often forego health insurance due to the expense. If you lose (or leave) your job you’re eligible to keep your current insurance plan for 18-36 months with COBRA (Consolidated Omnibus Budget Reconciliation Act, which is such a ridiculous backronym that I had to google it just now). This is often the only time people realize the true cost of their insurance as the entirety of it is then passed on to them directly (at the employer negotiated rate) and it shows up as a new monthly bill.

I recently left my employer to start my own business and discovered that my true cost of insurance is ~$700/month ($660 Health/$42 Dental). Keep in mind, this doesn’t mean that I have zero medical bills should I actually visit a doctor or hospital. This is pretty good health insurance, but I still have to pay $5,000 out pocket (annually) before it kicks in at the full coverage amount. Since I had ear surgery earlier in the year and hit that limit, and wanted to be able to continue seeing the same doctors I had for already scheduled follow ups, I decided to keep the same insurance. That $5,000 isn’t the only expense that landed on my shoulders, there’s a bunch of rules that I honestly don’t fully understand and I’ve probably ended up paying somewhere between $7,500-$10,000 for the surgery I had (in addition to the monthly premium).

The main reason I keep paying insurance (in addition to the fact that you’ll now be charged a penalty on your taxes if you go uninsured for a month), is my fear that you mentioned in the original post. Having a car hit me while I’m walking down the street and ending up with a $50,000 visit to the emergency room is a very real possibility without health insurance. California recently limited ambulance rides to a maximum cost of $1,200, so that’s… good?

It is true that nobody pays the cartoonishly high bills that you see posted online. It is also true that we spend way more on healthcare than basically anyone else.

My company offers very good insurance. Anything "in network" is free after the first $3000 every year, and the monthly premium is around ~$330. Note that this is a company that intentionally offers very good health insurance so they can be less competitive when it comes to salary and time off. I'd say in a given year, I spend around $7,000.

But really, one of the biggest practical issues with our healthcare system is its opacity. Most people are unable to figure out what most things will cost them before they consent to care.

A lot.

Back in 2007, I had just finished college and was traveling cross country to start a new job. I had to stop and get emergency surgery on the way there and ended up in the hospital for a few days. I ended up paying around $70,000 over the next few years and the hospital finally forgave the rest of the bill.

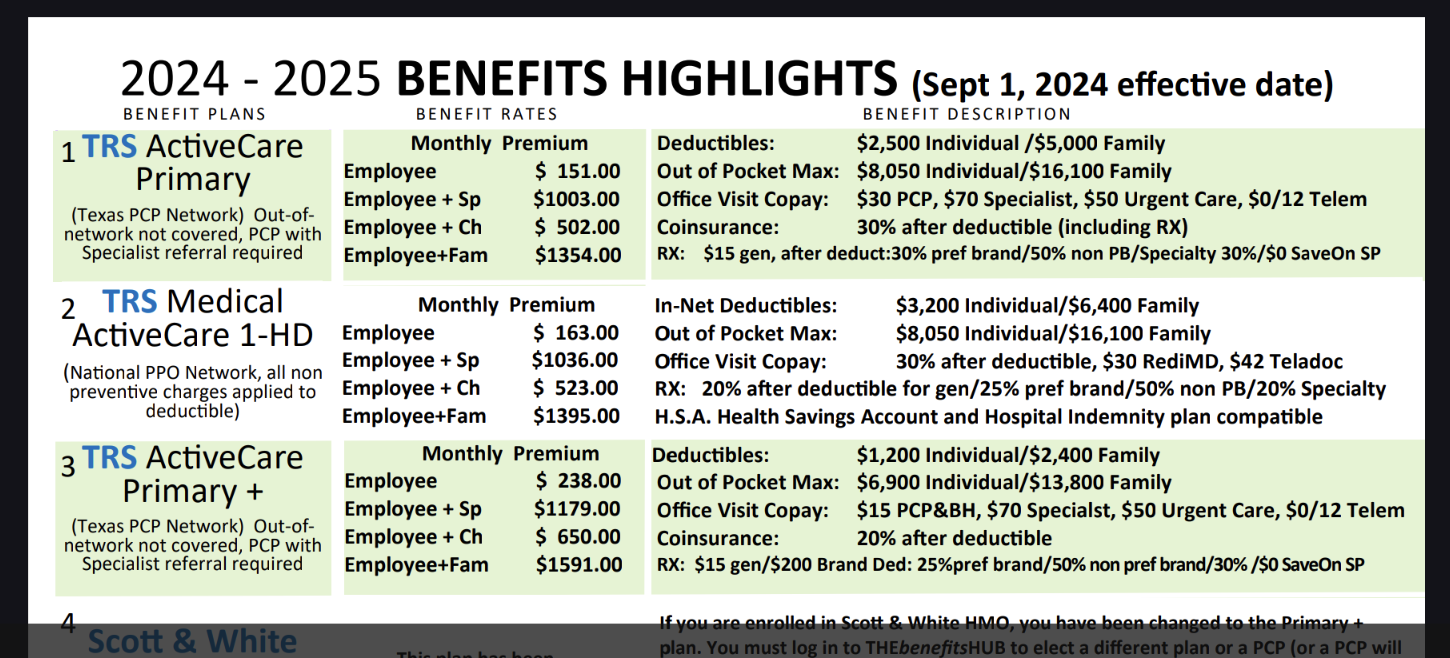

I work for a public school district. We're signing up for insurance now to begin sept 1. These are our available plans. I always take the HD (high deductible) plan because i contribute to an HSA (health savings account- pretax money that you put into an account. They send you a card and you can use that to pay med expenses.)

ETA- forgot to finish my thought- I may switch to the higher plan because i see it's only $75 per month more but saves $2k in deductible and $1100 out of pocket max. I'm considering a knee surgery this year, so i would likely meet those. This is an area where you have to pay your bill if you want to ever go back. I still owe $700 to the anesthesiologist for the other knee surgery 3 years ago. I will have to pay that to schedule another. For emergencies, hospitals are required to treat. My son without insurance had an emergency appendectomy 5 years ago and has never paid a dollar of the $5k he owes. They continue to send bills and he continues to throw them away. If he had another emergency, he could show up at the ER and they would treat him and the cycle would continue forever until he needed a scheduled procedure with that hospital system. Then they would likely require that he pay a certain amount upfront. My other son has obamacare. He pays $250/mo for it because he sees a weekly therapist that's $75 without insurance or $20 with insurance. It's all a very complex game of which is cheaper, what are you getting, how much are you willing to risk/commit, and do you expect to get sick or have an accident. My husband cannot add me to his insurance because i have access to it through my work. I was on his dental insurance and they dropped me because we couldn't find our marriage certificate from 30 years ago. 30 years of tax records showing we filed as married were not sufficient. It's really just their way of getting spouses and families off the plan. It's all a scam.

I pay $30 per doctor's visit and $40 if the visit is for a specialist. I also pay $0 for a yearly checkup and $0 for telehealth. For any hospital visits, I pay 20% of whatever the actual bill is after a $300 copay (basically a down payment), which came out to a total of $600 when I went to the ER. Lastly, my prescription drugs are capped at $10 per month for generics and $150 for some brand-name drugs.

I use a ton of healthcare and the costs have been super manageable, but affordability is going to vary wildly between people. A ton of insurance plans don't start working until you hit an out-of-pocket minimum of several thousand dollars, and others work like mine except with way higher copays.

Lastly, insurance often doesn't cover certain drugs or procedures. As someone with really good insurance with good customer service, it's still an issue every so often, and the solution is either to find an alternative, try to find a manufacturer's coupon and pay up, or suck it up and move on. There are insurance companies that use shady tactics to get them out of paying for certain expensive drugs that they're supposed to cover.

Dragoneer?

Yep. It's outrageous to me that the largest fee listed on his gofundme is medical bills.

Currently, nothing.

If your income is low enough, you can get free insurance through the government. In my experience, the regular doctor checkups and stuff is covered, along with prescriptions and any emergency room visits. The dental portion only covers the worst dentist in town, and vision is non existent.

It's not great, but medically necessary things are covered without copay or arguing with an insurance company to get it paid for. It's good enough that I've known people who purposely kept their income low to continue to qualify for the free insurance.

I have good insurance. I pay $20 per paycheck for my wife’s coverage. Our typical visit costs 20-35 depending. Our medications cost 10-20 per 3 month supply.

Most people don’t have insurance this good.

It really depends. Some people have insurance that limits their liability to $500 or whatever for hospital visits, but if so they probably are paying a lot out of each paycheck for that.

I have family coverage and this plan pays essentially zero towards anything, except pays 100% of the annual wellness visits to GYN, GP, and dermatologist, any vaccines considered preventative too. Then there is a "deductible " of 6,850 per person with a maximum of 8,000 a year, then it would then pay 80% of anything above that $8k until we paid $16k, then it would cover 100% of anything above that. So basically it really is "insurance" not healthcare.

Which would be ok except that the plan itself costs almost $7k a year in premiums. I am not getting that much value out of it. And that's not even the total, my employer is paying some too!

So most years this costs us in total maybe 8,000, the premiums plus a couple of visits and any drugs.

The only people winning in this system are the insurance companies, the one who owns our plan made revenue of $371 billion last year and a net PROFIT of $22 billion.

Oh and as you are asking about uninsured, I was for a long time, and you have to negotiate your own prices in that case, argue for a cash price. And hope nothing big happens. The mammogram cost almost $600 when I had to get a diagnostic one, colonoscopy $1,500. Childbirth, at home with midwife including all prenatal about $8k. Doctor visits between $80 and $200.

How do you pay for car insurance or renters insurance? It's not too dissimilar to that.

Though, I've moved to a state that has deemed me poor enough to give me Medicaid so the taxpayers pay for mine weather I want it or not. It beats paying almost $800 because living with my mother disqualifies me from the affordable care act subsidy.

Firstly, thanks everyone for all the responses. I appreciate it, and I hope that some of you felt better after having a vent.

American friend predictably says there's a problem with "healthcare literacy" and that you just don't have to pay the bills and they probably won't chase it up. I don't beleive that at all.

I figured it might be interesting to share how much I pay for stuff up here in Scotland.

I have a decent well paying job so I pay some money to the NHS in taxes, specifically ~£2000 a year. I get antidepressants and doctors appointments completely free from that. Dental I don't get free because my income is too large, but it's only like £20 for most routine things. I have a free eye test booked next week, and I splurged £10 extra to get fancy 3D imaging stuff done.

I do require mental health treatment though, and the NHS doesn't cover that for autistic people (as a competence issue, rather than a policy choice). A session with a counsellor costs £45 per hour for me privately.

Honestly, the surprising thing to me isn't that you have an insurance system (Switzerland has a similar thing, iirc), it's just how inflated prices are compared to here.

American friend predictably says there’s a problem with “healthcare literacy” and that you just don’t have to pay the bills and they probably won’t chase it up. I don’t beleive that at all.

healthcare literacy is an understatement and i'm glad you quoted it, you literally have to be a full time lawyer reading through this shit with a career SPECIFICALLY in handling health insurance to be able to understand it. Outside of that you're literally just guessing that it'll work.

Maybe someday i or someone else can found a thing like "open healthcare" providing that information for free in a fully publicly accessible manner. Why it isn't legislated, i don't know.

I quit even responding to them. After two or three years I'll get sued for a very small amount. It will be some radiologist who looked over a xray who has sold his debt to some bottom feeders. I wait until I'm served then I pay it. Within six months some other bottom feeder will serve me again for the same debt. When I go to court showing it was paid I can generally get my money back from the second bottom feeder. I've done this three times and got paid twice. The third time cost me nothing but time. Its long drawn out and stupid but its the shit sandwich we are forced to eat to live in the Home of the fee.

You essentially gamble a little bit. Most people get insurance through work (or they are part of a family plan). Generally, you'll have a few plans to choose from. If you are older, or have recurring issues, you might pick a plan that's a little more expensive, but covers more costs. If you are young and healthy, you might pick a cheap plan, essentially betting that you won't really need healthcare other than your yearly checkup and some vaccines.

The biggest thing with healthcare in the US is that it's very complex. Even if you have insurance that should cover something, it can be hard to find a doctor that's part of your insurance, so people often put off going to the doctor, which is part of the reason why costs are high. Teeth and eyes have separate insurance cause they are optional, apparently.

You basically have "premiums" that are your monthly payment. If you get your insurance through work, they cover a percentage of that; generally a pretty hefty amount of it. They usually don't outright tell you what percentage, though, so many people think insurance is cheap, and get a rude awakening when they lose a job, and suddenly can't afford $1000 a month when they used to be paying $100. Those premiums are taken out of your paycheck pre-tax, too, which gives you even more of a benefit if you have a job.

Depending on the "style" of the plans, they cover things differently. They all (I think) cover "preventative care" completely, which includes your yearly checkup, vaccines, and birth control for women. After that, some plans have "co-pays", which are set costs for a few things, like $25 for a normal doctors visit, $50 for a specialist, $100 for an emergency room visit. Some just cover a percentage of those costs, and some don't pay anything until you hit a limit (the deductible). Finally, there's an "out of pocket" limit. That's most you'll have to pay in a year, after which point the insurance covers everything.

All together, I pay less than $1000 a year for healthcare, but if I got really sick, and needed a bunch of expensive healthcare, I would quickly hit my out of pocket maximum, which I think is like $6,000. I could cover that, but many people cannot cover an expense like that on short notice.

The number on bills is very misleading. The hospitals know that insurance will negotiate down, so they start high, and then after the negotiations, insurance will pay some or all of the remainder. If you don't have insurance, you typically don't pay that whole number on the bill, either, cause the hospitals recognize that they dont have to adjust it up for the negotiation. You can still negotiate on your own, though.

A lot of it depends on what insurance you have and what insurance you have depends on who you work for.

I had EXCELLENT coverage with Kaiser Permanente, and other than a couple of hundred dollars a pay check and an in-office co-pay for treatment, I never had a bill.

When I had my heart attack, the Emergency Room was $150. 8 days in the hospital and open heart surgery from the head of the department was $100. The prescriptions and all the oxygen bottles I could carry was $100.

4 weeks into recovery, my company got bought. :( The new company didn't do Kaiser in Oregon. If I lived in California or Washington, I would have been fine, not Oregon.

So they switched my insurance to Aetna which meant I lost all of my doctors and had to start over at a new hospital. Kaiser is members only and I was no longer a member.

Naturally I started having complications, congestive heart failure. That was an ER visit followed by 7 days in the hospital.

Under the new insurance, they start by paying 80% and there is an out of pocket maximum of $6,500. Once you pay that, all other treatment is free the rest of the year. No co pays, nothing.

So I hit my $6,500 about 1/2 way through January. Goodbye signing bonus! But all the other complications I had the rest of the year were covered 100%.

Now... if I had NO insurance? 15 days in the hospital x 2 hospitals? Open heart surgery? All the tests and such? 24 oxygen bottles? A million dollars, maybe more?

Please don't post about US Politics. If you need to do this, try !politicaldiscussion@lemmy.world

1) Be nice and; have fun

Doxxing, trolling, sealioning, racism, and toxicity are not welcomed in AskLemmy. Remember what your mother said: if you can't say something nice, don't say anything at all. In addition, the site-wide Lemmy.world terms of service also apply here. Please familiarize yourself with them

2) All posts must end with a '?'

This is sort of like Jeopardy. Please phrase all post titles in the form of a proper question ending with ?

3) No spam

Please do not flood the community with nonsense. Actual suspected spammers will be banned on site. No astroturfing.

4) NSFW is okay, within reason

Just remember to tag posts with either a content warning or a [NSFW] tag. Overtly sexual posts are not allowed, please direct them to either !asklemmyafterdark@lemmy.world or !asklemmynsfw@lemmynsfw.com.

NSFW comments should be restricted to posts tagged [NSFW].

5) This is not a support community.

It is not a place for 'how do I?', type questions.

If you have any questions regarding the site itself or would like to report a community, please direct them to Lemmy.world Support or email info@lemmy.world. For other questions check our partnered communities list, or use the search function.

Reminder: The terms of service apply here too.

Logo design credit goes to: tubbadu